From Houston Agent Magazine

More housing inventory and lower interest rates are on the horizon, which should give the real estate industry a jolt, Lawrence Yun, chief economist for the National Association of REALTORS® (NAR), said this week. Specifically, Yun expects a pre-election interest rate cut this fall — the first of six to eight rounds.

So, what does this mean in the coming months?

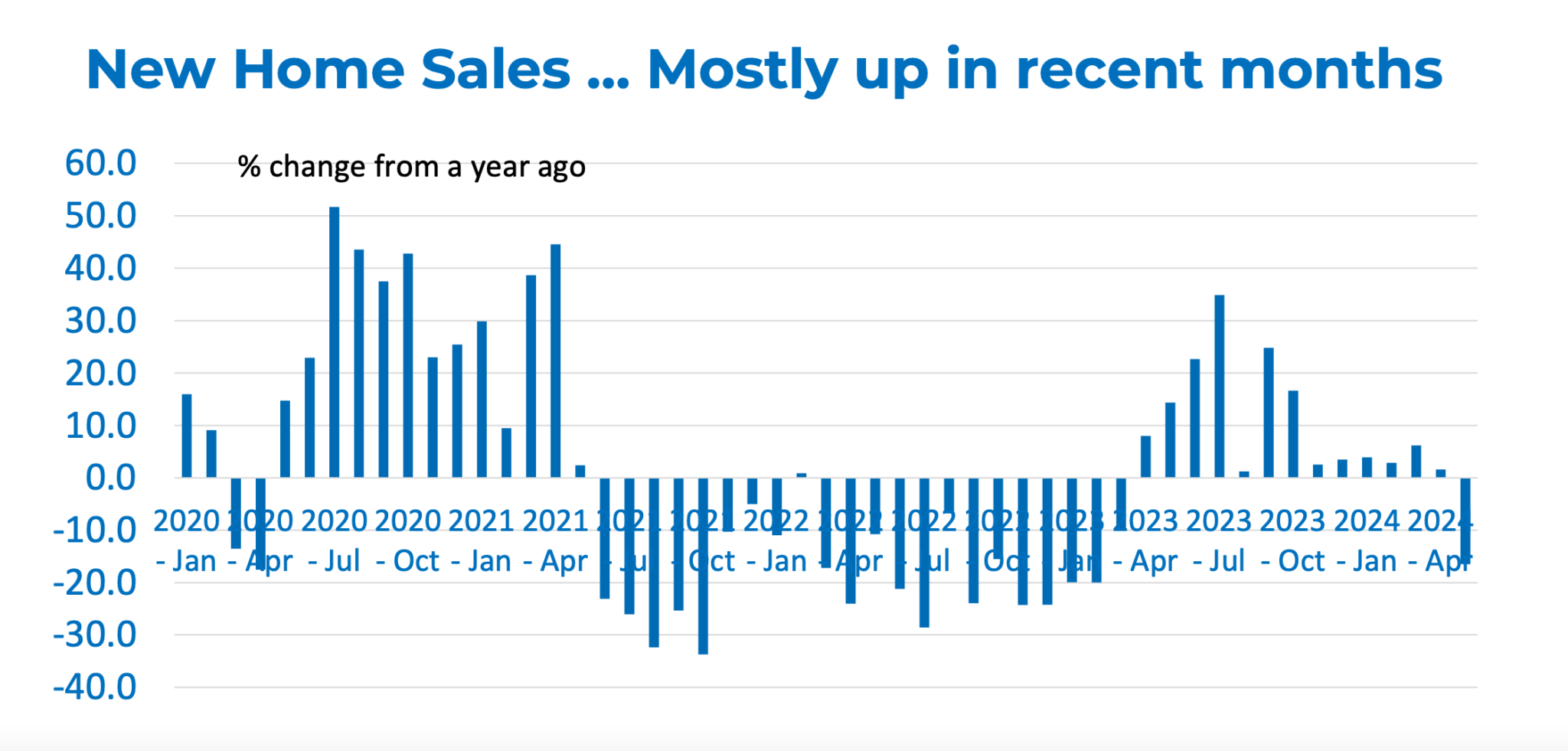

New and existing home sales

Speaking at NAR’s Real Estate Forecast Summit on June 22, Yun stated that both existing- and new-home sales are both hovering around last year’s levels. But when you compare the numbers to pre-COVID data, new home sales show significant traction.

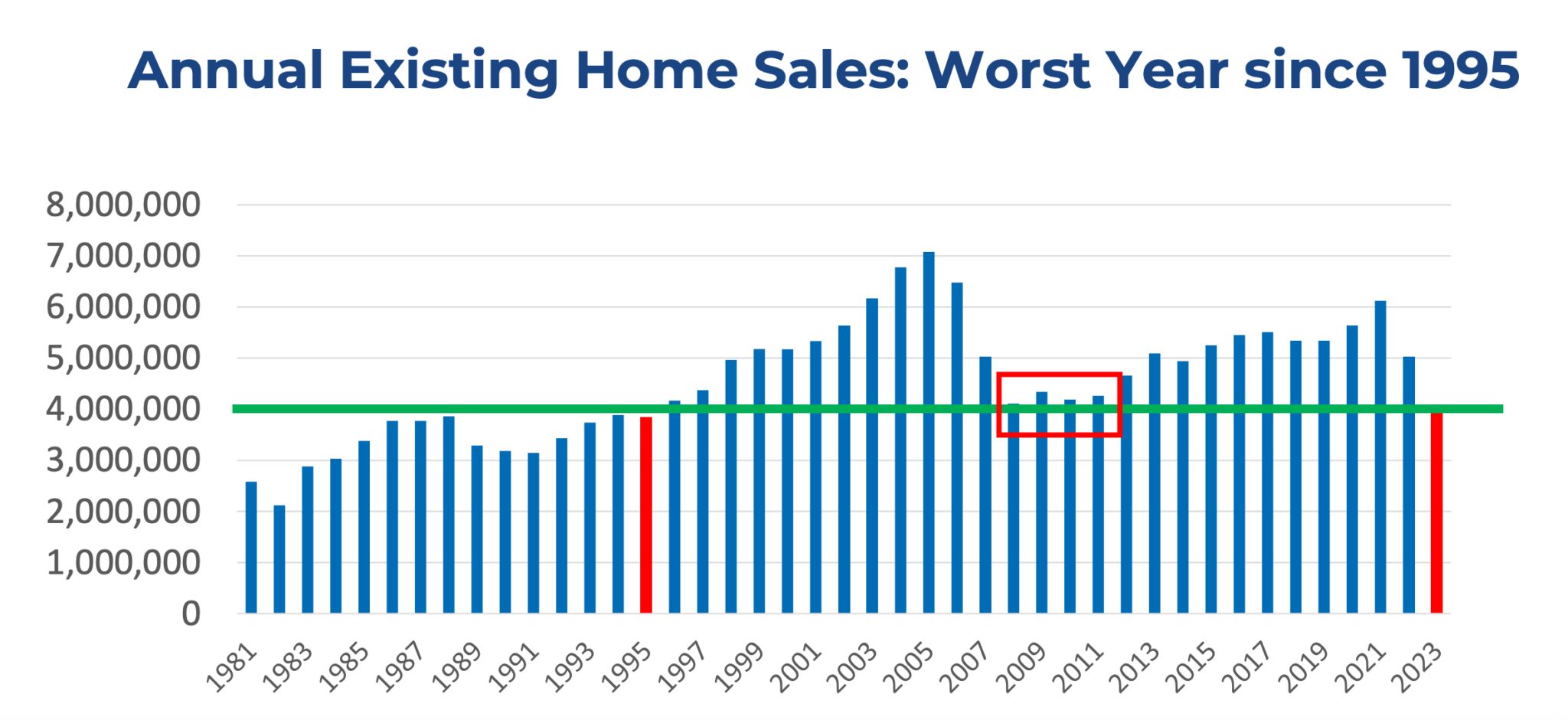

First, Yun noted that last year was “not good” for home sales. Realtors know this. In terms of existing-home sales, 2023 marked the lowest year since 1995. But Yun stressed that the near-0% change is “comforting.” In particular, the new-home market displays serious positivity as builders do not have to worry about the so-called “lock-in effect,” which Yun says dissuades current homeowners — who purchased with low interest rates — from selling.

He then highlighted the year 2020, an unusual one to be sure, before zooming out. In 2020, 5.64 million existing homes were sold, and 822,000 new homes were sold. That represented a big bump for both home types. In 2021, too, existing-home sales rose even more substantially, hitting 6.12 million, while new-home sales decreased somewhat to 771,000.

Both home types declined since then, with 4.09 million existing-home sales and 666,000 new-home sales occurring in 2023. But looking back to consider earlier data, new-home sales are still higher than they were in 2017. Three years before the onset of the pandemic, just 613,000 new homes sold. Compare that to existing homes — 5.51 million sold in 2017 — and one can conclude that, despite the post-pandemic, higher-interest-rate slump, new home sales are on the up.

That pattern holds true in 2024, save for a recent drop in May. “Interestingly, for the past 12 months, for the most part … sales were rising, because [builders] were able to create inventory … they just have the think about the buyers — more inventory to get more sales done,” Yun said.

A historic analysis

In 2023, when existing-home sales reached record-low levels, they closely mirrored the recession years of 2008, 2009, 2010 and 2011. “But the big difference is that during the Great Recession, people were losing jobs, people did not have income… they could not buy homes. But today, we are creating jobs, yet we are not getting home sales due to the lack of inventory.”

Since home sales hit a low point in 1995, the U.S. population has grown by 70 million. “U.S. population always rises by to 2 to 3 million each year, due to the birth rate outpacing death rate, and then we have immigration,” Yun explained. “So how is that we have 70 million more people, yet home sales are this low?”

Naturally, the answer comes back to high interest rates and low inventory.

“But,” he continued, “just imagine, if the interest rate was to decline and we have more inventory, how 70 million people could add to the housing demand and more transactions … [So much] pent-up housing demand could be released into the market should conditions improve.”

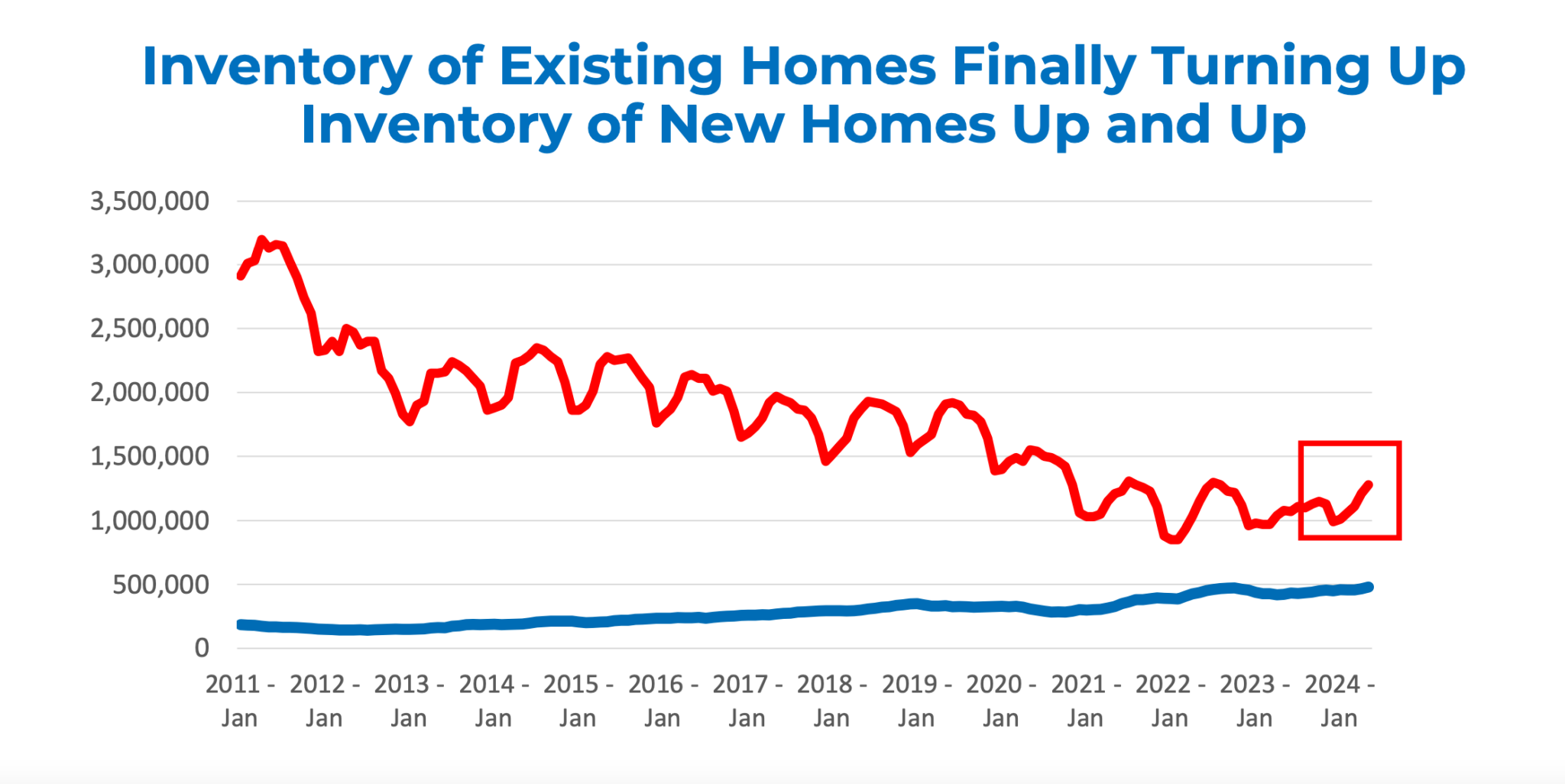

Red is existing-home inventory; Blue is new-home inventory, via NAR

Yun expects both of those conditions to improve somewhat soon. Citing recent data on existing-home sale inventory, “which is what Realtors are really focused on,” he said that there is about 15% to 20% more inventory now compared to one year ago. And while the new homes represent a much smaller market share, those numbers are rising too. “This is an early indicator that we may finally begin to start seeing more home sales,” Yun said.

Home and rental prices

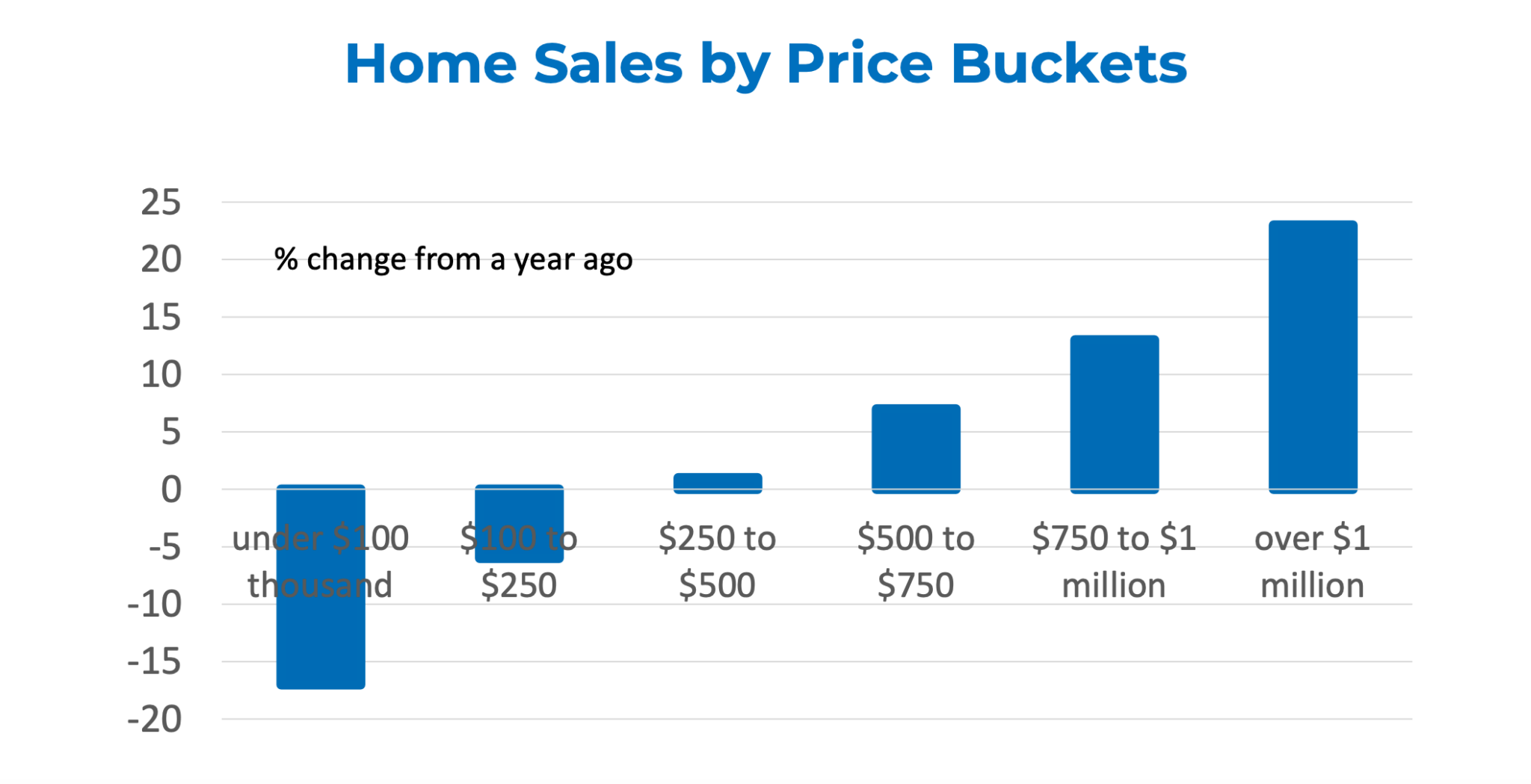

With supply rising, home prices are beginning to peter off. “If you have a listing, don’t expect prices to be 10% above one year ago,” he said. Some markets may even require a price reduction. By price bucket, there is more inventory at the upper end of the market, and, in turn, more expensive home sales are improving.

In general, though, there is strong appreciation nationwide from pre-COVID price levels. Yun highlighted states like Florida and Montana, where price growth is especially high; in Illinois, it’s somewhat average at 34.9%. And, because of those gains, the home market is difficult for younger generations to enter. A median-priced home today requires a six-figure income to purchase.

Meanwhile, homeowners still maintain substantially more wealth than renters. Yun’s own estimate for the year 2024 shows that the typical homeowner will have $415,000 of cumulative wealth, compared to just $10,000 for a typical renter.

And things aren’t getting any easier as multi-family housing starts dwindle. At the same time, multi-family completions have grown, which might offer temporary relief to renters as rising rents stall. But, two or three years down the road, Yun expects rents to accelerate due to a new shortage. After all, it takes roughly two years for a multi-family building to rise.

The fading ‘lock-in’ effect

Citing general population characteristics, Yun expects the lock-in effect to diminish naturally, and steadily, as delayed sellers will no longer be able to wait any longer to move. For example, over the last two years, 7 million babies were born. “If [parents] need a larger size home, they will need to list their starter home,” Yun said. Meanwhile, the same number of Americans, 7 million, reached retirement age, which often constitutes a residence change.

Additionally, there were 50 million job switches in America during that time, plus 6 million net new jobs. “[Those] people now have different commuting patterns. For how long are they going to hold on to their old home, at 3%, and not seek out a new home that better suits their commuting patterns?” Yun asked. Without the lock-in effect, he said we would have 1.5 million more home sales right now, Yun said, citing a recent Federal Housing Finance Agency analysis.

These stats indicate “the right conditions,” according to Yun, adding that, “We’ve turned a corner.” So, the next concern is interest rates.

The Federal Reserve has maintained near-7% rates for a over a year now, and the same question is on everyone’s mind: “When will the Fed cut interest rates?” The original plan was for the Fed to cut interest rates once inflation reaches 2%, Yun said — we’re not there yet. The consumer price index (CPI), which measures inflation, was 3% in June.

Despite steady deceleration, Yun offered another possibility. “There is an expectation in Wall Street that there could be an interest rate cut this autumn. It’s likely to be pre-presidential election, but the Federal Reserve is making their decision completely independent of political factors,” Yun said. “I know some of you will not believe that but as an economist … I would say that if the Federal Reserve was to cut interest rates in September, they would be doing it based on economic reasoning.”

In addition to rents coming down, which will encourage the Fed to cut rates, “Something else the Federal Reserve isn’t talking about, they don’t want to talk about it, is [that] some of the regional and community banks are still hurting. Commercial real estate loans and office lending loans are souring. Their balance sheet is not great. The only way to help out the community banks is to cut interest rates.”

More specifically, Yun expects these eventual cuts to occur before 2025 across six to eight rounds. In turn, he says, home sales will improve “somewhat” in second half of 2024 then, in and after 2025, a sizable population with pent-up demand will be there, waiting, for when inventory grows further.

“Maybe eight of the next 10 years will be improving years,” Yun concluded.